How Does The MannKind Story Compare? 2/16/16

*** The February issue of Nate’s Notes was published for subscribers earlier this month, but is now available for the general public below; however, please note that all recommendations are as of February 5 and therefore may now be out of date. ***

ISSUE 253

February 5, 2016

Did you hear about the termite who

walked into the pub and asked

“Where’s the bartender?”

– from The World’s Best Supersonic Riddles

Someone Buy This Newsletter A Drink!

Wow! It is hard for me to believe, but Nate’s Notes is turning 21 with this issue (hence the call for a drink)! Unfortunately, as you will notice as you read through this month’s issue (and with a few notable exceptions here and there), I am afraid there is not much else going on for us to celebrate this month…

As you can see in the Eyebrow Levels table below, the markets are continuing to slide, and while it would be great if there were only bull markets, if there’s one thing I’ve learned in the time I’ve been doing this, it is that bear markets are an inevitable part of the equation, and rather than fight them, our job is to step back and respect them.

Though it is quite possible the markets will start rallying on Monday and never look back, I have to admit that I am feeling somewhat relieved that, at least for now, it appears it was the right thing to do to move some cash to the sidelines last month… and, as you may have noticed, we are moving roughly another 10% to cash in the Model Portfolio this month (and reducing our margin debt by a bit in the Aggressive Portfolio as well).

After all, history suggests we may be entering a period in which those investments that have been working suddenly stop working… and those that haven’t been working (but “should have been”) finally start to… and, as you will also notice, along with lots of “sell” orders, I am also being fairly aggressive with some our purchases of stocks/ETFs that match that criteria this month.

Though space is short this month since I want to talk about MannKind “in earnest” (for what will hopefully be the last time – I really would like to get back to not needing to comment on rumors every month, but we’ll see what Fate has in store!), I want to remind you that most stocks actually only trade at “fair value” for a small fraction of their lives, with the rest of the time spent trading back and forth between undervalued and overvalued… and the more extreme a stock tends to get at one end of the spectrum, the more extreme it is likely to become at the other end as well… and this is especially true when it comes to biotech (so keep that in mind as you compare and contrast the likes of Celgene and Illumina with MannKind, for example… or what’s going on with Apple and many of the chip stocks, for that matter. To repeat one of our favorite mantras in the newsletter, “once trends get underway, they often go on for far longer than seems reasonable”).

My Latest Thoughts On MannKind (MNKD – $0.97)

Though the list of topics and rumors that could be discussed is virtually endless, I want to use this month’s update to first touch upon some of the more pertinent things that came up in the company’s conference call last week, and then to spend some time putting the current situation into perspective for everyone.

First off, it should be noted that while MannKind and Sanofi are hoping to have everything wrapped up by April 5th, CEO Matt Pfeffer noted that it is a very complex situation to unravel, and thus, it may take a bit longer before all the details are worked out; unfortunately, this means that MannKind’s hands are tied until then with regards to actually implementing any changes in the strategy for Afrezza going forward (including filing for approval in foreign jurisdictions) since Sanofi is still the holder of all rights associated with the commercialization and distribution of Afrezza.

That being said, once Afrezza has been fully returned to MannKind, Pfeffer confirmed that while the company is exploring the possibility of finding new partners who may be interested in adding Afrezza to their own product line-ups, MannKind is also moving forward with plans to market and sell Afrezza on its own (at least in the U.S. as part of the initial “next steps” the company is planning to take).

Moving on to other applications of the Technosphere (TS) platform, I am afraid that very little new information was revealed about the “mysterious” Receptor Life Sciences (RLS), the Seattle-based company that recently signed an agreement with MannKind to utilize the TS platform for the development of a number of proprietary compounds that are being worked on by RLS.

As you may or may not know (depending how closely you follow the story), the folks behind RLS have chosen to keep their identities confidential for the time being, though Pfeffer was able to confirm that they are a completely separate entity from Al Mann and MannKind (rumors abound that Paul Allen is behind RLS, but, as far as I know, no definitive evidence has been found yet to confirm that rumor). In addition, Pfeffer also acknowledged that one of MannKind’s most prominent scientists is now the Chief Science Officer at RLS (and has been there for awhile, it seems).

Along with the above, MannKind also spent a good portion of the call providing an update on the projected timelines for development of the TS applications that the company has been working on for awhile now, and management also took some time to remind folks of just how deep the company’s patent portfolio actually is.

And, now that you’re up to speed on some of the main highlights to come out of last week’s conference call, I hope the following discussion will help you best figure out how to best approach the story from an investment perspective…

First off, as indirectly mentioned above, I think it is important to recognize that “fear” and “greed” really are the two primary forces that drive stock prices over shorter time-horizons, and this is especially true when it comes to the biotech sector. In addition, I believe it is worth noting that the stocks that overshoot by widest margins at one end of the spectrum are often the ones that overshoot by an equally large margin on the other end of the spectrum as well.

And, as you might imagine, if I felt that the stock was undervalued when it had a market cap of $2 billion a mere six or seven months ago, you know I consider it to be extremely undervalued with a market cap of just over $400 million today (and that’s after already doubling off the extremely, extremely undervalued market cap of just $200 million that was touched last month right after it was announced that MannKind and Sanofi would be parting ways!).

I know it is hard to battle your emotions when it comes to evaluating stocks that have done nothing but hurt your portfolio, but I hope everyone will keep the following things in mind as they try to figure out what to do next…

First off, as always, please do not own more than you are comfortable losing – there are no sure things in the stock market, and we are far from being “in the clear” when it comes to the MannKind story.

Second, while short sellers like to stir up fears that the company will soon be filing for bankruptcy (which is, admittedly, a possibility), there are plenty of other routes the company could take that would be both easier and less painful than a bankruptcy filing… and thus, I am not terribly concerned that this fear will come to pass.

However, I DO have some concerns (and would be remiss if I didn’t point out) that rather than sink into bankruptcy, the company could be taken private “for a song”… and though such a turn of events would be both nefarious and completely out of character for Al Mann, it probably ranks the highest on my list of “things to worry about when it comes to the MannKind story.”

Having said that, one of the things I hear most often from new subscribers is “I really wish I would have been a subscriber when you first recommended Celgene (or Apple… or Illumina… etc.),” and, while I cannot promise that the MannKind story is going to work out as well for us as those others have (and with the recognition that we have been in the stock for awhile now, so many of us are “averaging down” at current prices rather than starting new positions), I do want to remind folks of what was going on when we first got involved in some of those stocks in order to help give you some confidence that there may, in fact, be some hope for MannKind after all.

Though I had been following Celgene for a number of years before recommending it in the newsletter, it had spent much of that time as a bioremediation company focused on using microbes to clean up toxic waste sites; however, the management team at Celgene had recently come across new research that suggested that the infamous drug thalidomide was showing potential as both a treatment for cachexia (a “wasting syndrome” associated with a number of illnesses, especially AIDS), as well as certain types of cancers.

Not surprisingly, the stock suffered greatly as everyone who had been owning it to be involved in bioremediation had to decide whether to sell it or to stay involved as the company began the transition over to being a pharmaceutical company – and, not just any pharmaceutical company, mind you, but one with no experience selling pharmaceuticals… that was going to attempt to break into the highly competitive cancer arena… by attempting to “bring back thalidomide,” a drug that had been banned for causing birth defects in just about every instance that it had been prescribed for pregnant women while it was on the market… and it was going to try and get into the business on its own, with NO partner.

When I first added Celgene to the newsletter in November 1995, despite already being up close to 150% for the year, it still had a market cap of just $87 million… and it went on to spend a number of years testing our patience while trading back and forth between $5 and $12 (or roughly 20 cents and 50 cents in today’s split-adjusted stock!) before it finally took off. However, though it took time, all of the skeptics on Wall Street who had been openly mocking the company’s plans to both “go it alone,” as well as attempt to market a product with a “black box warning” on the label that was perhaps the worst the world had ever seen (Celgene actually developed and patented a whole new method for doctors to discuss and address the risks of such a product with their patients as part of getting the product approved!) eventually came around as the results being obtained with the product began to speak for themselves… and the rest is history.

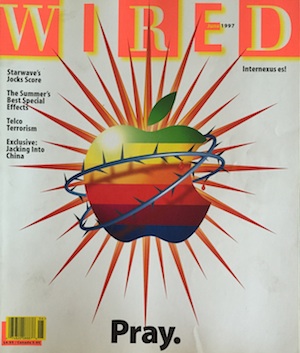

Along similar lines, though I had been familiar with Apple for many years, it was not until March 1998 that I finally added it to the newsletter (after it had already doubled off its lows, mind you!). At the time, it had also become a bit of a joke on Wall Street due to the success being achieved by the likes of Dell, Compaq, and other companies that were selling PCs running Microsoft’s Windows operating system. Not only was Apple’s market share dwindling to low single digits in a hurry, the company was also desperately strapped for cash in the ‘96-’98 time period, and many investors were concerned it would have no choice but to file for bankruptcy… and because I happened to come across it while cleaning out my garage this week, I thought it would be fun to share with you the cover of the June 1997 issue of WIRED magazine. As you can see, the outlook at the time was “grim,” to say the least!

Along similar lines, though I had been familiar with Apple for many years, it was not until March 1998 that I finally added it to the newsletter (after it had already doubled off its lows, mind you!). At the time, it had also become a bit of a joke on Wall Street due to the success being achieved by the likes of Dell, Compaq, and other companies that were selling PCs running Microsoft’s Windows operating system. Not only was Apple’s market share dwindling to low single digits in a hurry, the company was also desperately strapped for cash in the ‘96-’98 time period, and many investors were concerned it would have no choice but to file for bankruptcy… and because I happened to come across it while cleaning out my garage this week, I thought it would be fun to share with you the cover of the June 1997 issue of WIRED magazine. As you can see, the outlook at the time was “grim,” to say the least!

Of course, thanks to the fact that Steve Jobs returned to Apple and helped get the company back on track towards only putting out products that were head-and-shoulders above anything else on the market when it came to user experience and satisfaction levels, not only did the company survive, but it went on to become even more successful than just about anyone could have imagined due to some variation of the maxim that “happy customers make for happy shareholders.”

As it stands (and again with the acknowledgement that the successes of Apple and Celgene in no way guarantee the success of MannKind), I want to remind those of you who have come this far that many of the greatest investments of all-time have come from periods of market inefficiency like the one MannKind is experiencing right now. If you are new to the newsletter, I believe you are being given a once-in-a-lifetime chance to start a position… and if, like many of us (myself included), you have ridden the stock down from higher prices but are still involved in the story, the mathematics of the situation strongly suggest that you should be taking advantage of the situation to “average down” if you’re able to (and again, only to a level that will still allow you to still sleep easily at night).

Will it be a challenge for MannKind to sell Afrezza without a partner? Yes – but it’s been done by others… and given the nature of diabetes and associated support groups, I think it will be a significantly easier task for MannKind to sell insulin on its own than it was for Celgene to sell thalidomide, for example! And, of course, if the company does sign up one or more international partners (especially in territories where FDA approved products can be fast-tracked), the rates of sales growth will likely be that much more impressive as word starts to spread.

As mentioned before, while I can’t tell you why Sanofi had such a hard time selling Afrezza, I can tell you that I am more convinced than ever that Afrezza will eventually become the mealtime insulin of choice, especially as more and more diabetics start to monitor their blood sugar levels in real-time (a trend that is already picking up steam as continuous glucose monitors become less and less obtrusive and easier and easier to use)… and, at least for now, owning MannKind stock is the only way to invest in the story.

Of course, there’s much more to the story than just Afrezza, and with MannKind’s old science officer (perhaps the world’s leading authority on TS?) now in charge of the work being done at RLS, it shouldn’t be long before a) development milestones start being hit, and, perhaps more importantly, b) the idea that TS is really just a platform that will eventually be tapped to improve the delivery of many, many different compounds will start to be validated.

Yes, it has been a bumpy ride… and, yes, there is still plenty of risk in the story. However, as mentioned above, if you’re still following along, history suggests that you should be taking advantage of the current situation to add to your position.

Summary of Orders Filled

Orders filled 1/11/16 – Sold 3,500 (15,000) AFFX @ 13.96; 450 (3,000) AAPL @ $98.53; 200 (750) CELG @ $103.03; 700 (4,000) CRUS @ $26.86; 600 (4,500) EA @ $64.21; 300 (2,000) FSLR @ $65.42; 125 (750) ILMN @ $165.71; 800 (7,000) LMNX @ $18.87; 10,000 MNKD @ $0.67; 750 (6,000) NVDA @ $29.68; 200 (1,500) NXPI @ $77.22; 750 (3,500) @ $16.81; 100 (1,000) DBA @ $19.83; 200 (1,500) DBC @ $12.45; 300 (2,000) QRVO @ $44.22; 200 (1,000) SWKS @ $66.05; and 200 (1,000) DIS @ $99.92 and bought (200,000) MNKD @ $0.67 and 75 (750) GLD @ $104.74.

Orders filled 1/14/16 – Sold 1,500 (10,000) AFFX @ $13.85; 100 (500) AAPL @ $99.52; 100 (500) CELG @ $105.62; 250 (1,500) CRUS @ $27.47; 200 (1,000) EA @ $64.48; 200 (1,000) FSLR @ $61.78; 75 (250) ILMN @ $175.11; 500 (4,000) LMNX @ $19.40; 500 (6,000) NVDA @ $28.67; 200 (800) NXPI @ $74.51; 250 (2,000) PERY @ $17.90; 100 (1,000) DBA @ $20.00; 200 (1,500) DBC @ $12.34; 200 (1,000) QRVO @ 39.42; 200 (1,000) SWKS @ $64.54; and 100 (1,000) DIS @ $99.11.

In addition, the Portfolios were credited with 101.9 (360.1) shares HQL from special distribution reinvestments on 1/8/16 and $852 ($4,615) worth of DIS dividends on 1/11/16 (we forgot to report the special HQL distribution last month).

Top Picks (for new money this month)

All else being equal (i.e. you already own “pretty much everything” in the newsletter), my top picks for you this month are:

Luminex (LMNX) – Yes, the sector is currently under pressure, but I believe the company’s current market cap may make it an attractive takeover candidate if the industry starts to consolidate.

MannKind (MNKD) – Ironically, parting ways with Sanofi may prove to be the best thing that has happened for shareholders in a long while!

SPDR Gold ETF (GLD) – Gold is due for some cooling-off, but I continue to believe that, at some point, it is going to make a monster move to the upside… and this move might be getting underway now that the stock market appears to be rolling over into a new bear market.

Outstanding Orders

For the reasons discussed above and below, the Model (Aggressive) Portfolio will sell 150 (500) Apple, 100 (500) Celgene, 150 (500) Cirrus Logic, 200 (1,000) Electronic Arts, 50 (250) Illumina, 750 (3,000) NVIDIA, 100 (400) NXP Semi., 100 (500) Qorvo, 100 (500) Skyworks Solutions, and 100 (500) Walt Disney and purchase 100 (500) First Solar, 300 (2,000) Luminex, 5,000 (200,000) MannKind, and 50 (500) SPDR Gold Trust ETF. We will use the closing prices on Monday, February 8th, for all transactions.

“Eyebrow Levels”

(used to help us gauge the overall health of the market*)

| current | one eyebrow | two eyebrows | |

| DJIA | 16,205 | 16,750 | 16,250 |

| Nasdaq | 4,363 | 4,500 | 4,200 |

| S&P500 | 1,880 | 1,950 | 1,800 |

| BTK | 2,743 | 3,200 | 2,700 |

| SOX | 586 | 630 |

580 |

*As long as all five indices are trading above their “one eyebrow” levels, it is a sign that the current uptrend is still intact; however, if the indices start to dip below those levels, it will cause me to raise an eyebrow and wonder if the trend my be coming to an end… and if both eyebrows go up, it will mean that things are deteriorating in a hurry (and you should start looking for a “Special Alert” from me in your email box).

Summary of Recommended Stocks

Affymetrix

Not surprisingly, Affymetrix’s stock has gapped up to the $14-level in response to the buyout offer from Thermo Fisher Scientific at that price that was announced just as last month’s issue was going to press. Since the deal is not expected to close until June, I have to admit that I am intrigued by the fact that the stock is actually starting to creep above the $14 mark… and, consequently, I am going to hold on to our remaining shares for at least another month just in case a higher bid happens to come in now that the company is officially “in play.” That being said, there is no reason for new subscribers to get involved, but existing shareholders may want to continue holding a bit longer. AFFX is a strong buy under $8 and a buy under $10.

Apple

For the company’s first quarter, Apple reported revenues of $75.9 billion and net income of $18.4 billion, or $3.28 per share, as compared to revenues of $74.6 billion and net income of $18.0 billion, or $3.06 per share, in last year’s first quarter. As discussed previously, though I find the stock very cheap at current prices, now that a new bear market seems to be getting underway, the odds are increasing daily that Apple’s stock is likely to experience another leg down in the weeks and months ahead as investors become more and more skeptical of the story; consequently, though I am still quite bullish on the company long-term, we are selling a few more shares this month. AAPL is now a strong buy under $85 and a buy under $95.

Celgene

Along with Apple, I am afraid that Celgene is an example of another market-leading company that is seeing its stock sag to levels that are no longer consistent with a “bull market” interpretation of its chart… and while it admittedly needs to fall just a bit more before it will officially signal a new bear market for the stock (and thus, the sector as a whole, almost certainly), I am taking a few more chips off the table here as well. For 2015, Celgene reported revenues of just under $9.3 billion and net income of $1.6 billion, or $1.94 per share, as compared to revenues of just under $7.7 billion and net income of roughly $2.0 billion, or $2.39 per share, in the prior year. CELG is a strong buy under $85 and a buy under $95.

Cirrus Logic

Thanks to a solid earnings report and some upbeat guidance, Cirrus’ stock has jumped dramatically in the four weeks since last month’s issue went to press! Unfortunately, however, I am growing more concerned that a new bear market may getting underway for both the sector and the market as a whole, and thus, despite the solid relative strength in the stock, I am selling a few more shares out of both Portfolios this month. For its third quarter, Cirrus reported revenues of $347.9 million and net income of $41.4 million, or $0.63 per share, as compared to revenues of $298.6 million and net income of $22.7 million, or $0.35 per share, in the same period a a year ago. CRUS is a strong buy under $25 and a buy under $28.

Electronic Arts

While it is true that if EA’s stock is able to hold above $55 in the days and weeks ahead, we will still be able to claim that the longest-term uptrend remains intact; however, when looked at over just about any other time-frame, I am afraid that EA’s stock has suddenly become a very bearish piece of evidence, indeed! Unfortunately, as discussed a number of times over the past couple of months, once downtrends get underway, they often go on for far longer than seems reasonable… and, though I continue to believe that EA is a stock we will want to hold a position in for many years to come, I am nevertheless taking a few more chips off the table as part of this month’s rebalancing. EA is now a strong buy under $45 and a buy under $55.

First Solar

Now that we have seen how the stock is responding in the current market environment (and admittedly after selling off 40-50% of our position in each Portfolio as part of the trades that took place between the January issue and today), I am repurchasing a portion of the shares we sold recently. Not only do I like the good relative strength that we have been seeing lately, I do believe that whenever trends develop “unexpectedly” (remember when “low oil prices are horrible for solar stocks” was a reliable mantra?), it is always worth thinking about being a bit more aggressive when it comes to positioning oneself relative to the trend… so that’s what we’re doing! FSLR is now considered a strong buy under $60 and a buy under $70.

Illumina

As you can see in the chart to the right, despite posting decent numbers in its most recent earnings report, Illumina’s stock has continued to slide in recent weeks and appears to be on the verge of breaking into new multi-year low territory (never a bullish sign). For fiscal 2015, Illumina reported revenues of $2.2 billion and net income of $461.6 million, or $3.10 per share, as compared to revenues of just under $1.9 billion and net income of $353.4 million, or $2.37 per share, in the previous year. Yes, I still believe the company is “best of breed;” however, as discussed elsewhere, there appears to be a new trend getting underway for the sector… so I’m selling a bit more. ILMN is a strong buy under $120 and a buy under $150.

Luminex

After popping nicely in response to the company’s most recent earnings report, as you can see in the chart to the left, I am afraid that Luminex’s stock has given back all those gains (and then some!). For 2015, Luminex reported revenues of $237.7 million and net income of $36.9 million, or $0.88 per share, as compared to revenues of just under $227.0 million and net income of $39.0 million, or $0.94 per share, in the previous year. While I am generally more inclined to sell biotech than buy it at the moment, I believe Luminex’s current valuation makes it a very attractive takeover candidate, and thus, it is one of the few stocks that I am actually buying this month. LMNX remains a strong buy under $18 and a buy under $22.

MannKind

As discussed above, whether you are new to the story or a battle-scarred veteran, I believe all signs are pointing towards the idea that you should be taking advantage of the current high levels of pessimism surrounding the stock to be starting or adding to your position, always staying at or below “the sleeping level” (the number of shares you can fall asleep easily with at night), of course. My gut is telling me that there will still be at least a few plot twists involving Sanofi and other potential players before all is said and done, but with a market cap of right around $400 million, I believe this situation has one of the most attractive risk-reward ratios most investors will ever see. MNKD remains a strong buy under $1 and a buy under $3.

NVIDIA

While “all will be fine” if the stock is able to hold current levels when the market opens on Monday… and then trade back up to the $32 in a hurry… I will be the first to admit that what was one of the most bullish looking charts in the newsletter two issues ago has now become yet another fairly compelling piece of evidence suggesting that a new bear market for both the semiconductor sector and the market as a whole may be getting underway. Consequently, despite my optimism about the company’s prospects over the long-haul, I am taking a few more chips off the table this month in an attempt to preserve our capital while Nature runs its course in the market. NVDA is considered a strong buy under $24 and a buy under $27.

NXP Semiconductor

For 2015, NXP reported revenues of $6.1 billion and net income of $1.5 billion, or $6.10 per share, as compared to revenues of $5.6 billion and net income of $539 million, or $2.17 per share, in the prior year. Unfortunately, as is the case with some many other stocks in the newsletter this month, I am afraid that NXP’s is also threatening to slip into new 52-week low territory… and if it does so, it will serve as yet another piece of evidence on the bearish side of the ledger. While there is a chance that the sector could be bottoming as I type this, experience has taught me that we are better off continuing to move cash to the sidelines… and so I am here as well. NXPI is now a strong buy under $65 and a buy under $75.

Perry Ellis

Though it is actually up a bit from where it was when last month’s issue went to press, I am afraid that Perry Ellis’ stock is also tracing out a chart pattern that is only growing more bearish-looking as time goes by. That being said, we have already sold off quite a bit of our positions in both Portfolios, and for this reason – along with the idea that Perry Ellis may be a takeover candidate if things do slow down and larger players start looking to buy up “smaller” players – I am going to hold off selling any more shares for the time being (though I will naturally be re-evaluating this position every month, and will sell more if circumstances seem to call for such action in the future). PERY is a strong buy under $13 and a buy under $16.

PowerShares DB Agriculture

While it is true that shares of this ETF appear to be finding some short-term support at the $20-level, a quick glance at the chart to the left ought to confirm that the longer-term trend is pretty clearly still intact. And, as you know if you have been a subscriber for awhile now, though I remain puzzled (and increasingly alarmed) by the fact that commodity prices are behaving in exactly the opposite fashion of how I thought they would be at this stage of the the game, I am also the first to admit that our job is to respect the trend rather than fight it… and though the contrarian in me has struggled at times, I think we’ve done a pretty good job of making sure that shares (continued under “DBC” below) DBA remains a buy under $20.

PowerShares DB Commodities

(continuing from “DBA” above) of both DBA and DBC have remained among the smallest of our positions during the course of the decline we have seen in commodity prices over the past couple of years. That being said (and with a recognition of the fact that “gold is its own special kind of commodity”), it will be interesting to see how the recent strength in gold ends up impacting the prices of other commodities (if it does at all). In the meantime, though I am adding to our gold position (based on the strength that has developed there), please note that I am going to hold off a bit longer when it comes to adding to our positions in the likes of DBA and DBC; however, for those of you anxious to buy, DBC is considered a buy under $12.

Qorvo

As you can see in the chart to the left, thanks to a variety of factors all coming together at once, Qorvo’s stock is scraping along just a couple of bucks above its 52-week low (which, if you recall, is technically also its all-time low, given that the stock was born out of the merger of TriQuint and RF Micro Devices a little over a year ago). For the company’s third quarter, Qorvo reported revenues of $620.7 million and a net loss of $11.1 million, or $0.08 per share, as compared to revenues of $397.1 million and net income of $87.7 million, or $1.18 per share, in last year’s third quarter (which, it should be noted, was when the two companies were both still independent). QRVO is now a strong buy under $32 and a buy under $36.

Skyworks Solutions

As you can see in the chart to the right, despite reporting a very solid quarter, Skyworks’ stock is yet another one in the semiconductor space that is threatening to start hitting new 52-week lows… and, as explained so many times before, since “trends often go on for far longer than seems reasonable,” our job is to try to own less of the stock during the downtrend (but to always hold an “investment position,” no matter what). For its first quarter, Skyworks reported revenues of $926.8 million and net income of $355.3 million, or $1.82 per share, as compared to revenues of $805.5 million and net income of $195.2 million, or $1.01 per share, in last year’s first quarter. SWKS is considered a strong buy under $55 and a buy under $65.

SPDR Gold Trust ETF

While gold is currently more than due for at least a short cooling-off period after the spectacular run it has made over the past four or five weeks (and it really needs to get back above $1,250/oz. (or thereabouts) before we could start to seriously consider the idea that a new uptrend may, in fact, be getting underway), because we try to only make trades once a month, I am raising the buy limits a bit and adding more shares to both Portfolios as part of this month’s “regularly scheduled rebalancing.” As always, while it is human nature to resist the idea of “paying up” for something, I want to remind you that you are encouraged to “buy strength” if you see it developing in the price of gold. GLD is considered a buy under $116.

Tekla Life Sciences Investors

Not surprisingly, as you can see in the chart to the right, HQL’s stock has been slammed along with the rest of the biotech sector over the past four weeks! And, while it is true that it is not fun to watch the shares themselves tumble, I think it is important to keep in mind that this closed-end fund is set up to invest in a broad cross section of the biotech sector… and this means that, provided the fund managers are on top of things, the current sell-off will actually set them up with an opportunity to take advantage of the bargain prices that are already starting to be created as part of the downturn. In the meantime, you are encouraged to be patient about new purchases. HQL is now a strong buy under $15 and a buy under $18.

Walt Disney Co.

Yes – if the stock can hold $90, I agree we could be looking at the possibility that a very significant bottom is being put in for the stock; however, if that level does not hold in the days and weeks ahead, I would be hard-pressed to not call it a very bearish signal, indeed. Given where I believe we are currently at in the fear-greed cycle, I will sleep much more easily at night if I take a few more chips off the table, and, unless you are just getting started with the newsletter (and are therefore still putting money to work to start initial positions), you are encouraged to join me in lightening up on your position until we get some evidence that the downtrend may be ending. DIS is now a strong buy under $85 and a buy under $95.